Founded in 1871, Svenska Handelsbanken (Handelsbanken) is one of the major banks in Scandinavia and Europe, it counts nearly 12,000 employees working in about 800 branches in over 20 countries. It is renowned for its strong culture, commitment to customers and management team that allocates capital in an intelligent way, with the right incentives and a long-term approach. It sets an example for banks worldwide while still retaining its Swedish conservative, traditional nature, a “strategic blueprint that other banks should aspire to follow”, according to a 2015 Berenberg report.

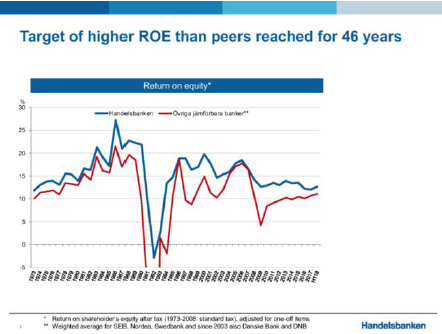

Former Chief Executive Officer (CEO) Jan Wallander brought organizational reform from 1970 onwards that has lasted until today by pioneering the decentralized banking method. Committing to a business model that is honest, value-driven approach has yielded positive results for the past four decades, even being more profitable than the average for other listed banks every year since 1972. Worth noting is that Handelsbanken never received any form of financial aid during severe economic recession or banking crisis, actually expanding its market share in the 1990s and since 2008 has delivered a higher total return to shareholders than any other big European bank. According to former President and CEO Anders Bouvin, ‘the ethos of the bank is: a bank should be an asset to the community, not a liability’.

Therefore, the question to ask is how was all this possible and what enabled such progressive outcomes? This was after all a bank, as traditional as one can get. After in-depth research and analysis, two clear factors revealed themselves as vital to the success of the Swedish bank – a very unique strategy and a strong internal culture.

Your Friendly Neighborhood Bank

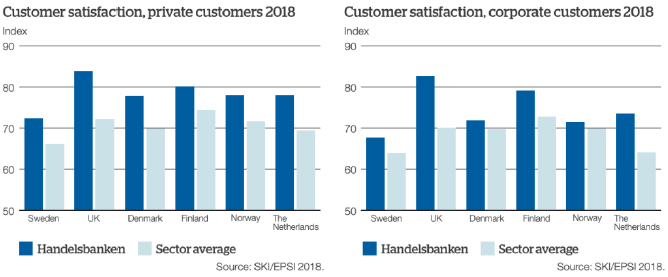

It wasn’t luck that got the bank ranked number one in customer satisfaction for the last 30 years and has the highest satisfaction levels with the digital services of Sweden´s big banks, as shown in the new EPSI report. Handelsbanken’s success is founded on its ‘localism’ ideology. Their differentiator is that they are a local relationship bank that is based on satisfied customers, financial strength and traditional values coupled with the ability to empower their people. Branch managers are granted a high level of autonomy in making their own decisions on their branch’s budget and every aspect of the branch’s banking operation.

Call centers, marketing campaigns and advertisements are shunned in favor of the personal touch. Whether they visit the bank branches or go online, customers are always given a bespoke service that directly addresses their individual needs and financial situation. Enter a postcode on the homepage and be taken to the local website where customers can meet the management team and read a message post from the branch manager. Introductions are made even before a face-to-face meeting, with continued interactions leading to strong customer loyalty and satisfaction.

By building a rapport between customer and branch staff, this can eventually develop into almost a personal relationship where the customer feels confident their interests are put first. When the bank understands their audience, they can deliver the right services and tailor products depending on what their customer’s individual needs are. The same goes for a local business running their accounts with their local Handelsbanken, since both understand each other which ensures there are benefits experienced by both sides. Business owners can breathe a sigh of relief, knowing they are working with a bank who cares enough to understand them, their business and whatever pressures and obstacles they may face along the way.

It is a practice built on trust.

“litar på dig” = “We trust you”

To truly deliver on its brand values, every staff member of Handelsbanken is committed to what the vision is. The shared beliefs of Handelsbanken aren’t encompassed in trendy buzzwords but instead a booklet simply known as ‘Our Way’ which was first written by Wallander in the early 1970’s and developed by new CEOs over the years. The booklet describes how to conduct banking operations. Dedication to the high decentralization philosophy even led to the unanimous removal of a CEO in 2016 when he resisted this decentralized approach, thus resulting in a culture clash.

Handelsbanken’s natural assumption is that ‘I trust first’. When the natural assumption is trust first and that people are empowered to take responsibility in the decisions they make, then an incentive plan or Key Performance Indicators (KPI) is unnecessary because employees will do the right thing by the business. Faith in employees leads to high levels of motivation and better quality of decisions.

What is interesting yet may seem provocative is that the bank refuses to hand out bonuses, financial incentives to do well and set targets for their people to meet. Instead, the bank asks their managers and staff members to exclusively focus on the customer needs. Fiscal rewards come to the employees in the form of equal share of profits when the bank’s return on equity beats their competitors.

Driving Digitalization in the Transformation Journey

For all that they are doing right, Handelsbanken is still encountering the same challenges every other company is in the new of Artificial Intelligence (AI). Their transformation journey needs to be structured around which decisions stay local and which decisions could benefit more with the help of technology or more centralization.

With centralization, the bank can ensure that their efforts aren’t duplicated and that the infrastructure is efficiently in place. However, there is also a risk of stifling innovation and slow reaction to new developments within the industry. Handelsbanken’s Chief Digital Officer understands the bank’s unique position and posits that transparency is key, noting that the worst thing to do is take away responsibility from empowered employees because it kills engagement. When engagement is already as high as it is in the bank, the challenge is how best to channel that untapped energy into productivity.

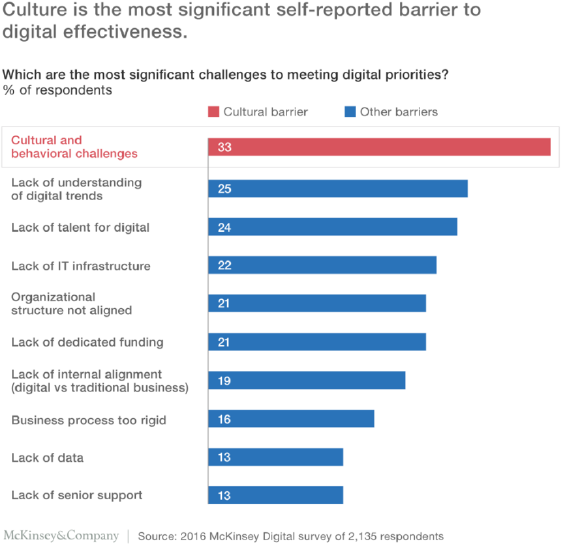

Culture is what guides decisions in the absence of policy

For personalized service, decentralization is crucial and how that is enabled is to build a culture of trust with a strong digital backbone. That is a given in Sweden, where even if the manpower isn’t there, everything is digital and data driven. Therefore, they invest more in culture and that is where there is more power in their strategy. By closely examining Handelsbanken, they are living proof that traditional business models don’t necessarily need a complete overhaul in order to achieve a multi-billion result. US$20 billion is not a bad market cap, the bank just has to make sure they don’t lose out in the game.

How traditional businesses adapt strategy and digital without disrupting but substituting and also complementing businesses, that is what is needed. The bank has the mindset they need to adapt and preserve the customer experience. Efficiency comes from digitization.

Financial Landscape in Malaysia

Perhaps the question to ask is if the basis of Handelsbanken’s culture is trust, can the same approach be applied to and replicated by banks in Malaysia? Financial technology (fintech) disruption is reshaping the industry along with external headwinds and uncertainties from Brexit and the trade tensions between the United States and China, among others. However, Malaysian banks remain resilient with reasonably healthy profits and asset quality. They have even weathered public perception affected by recent financial scandals and cybersecurity threats that have hit closer to home.

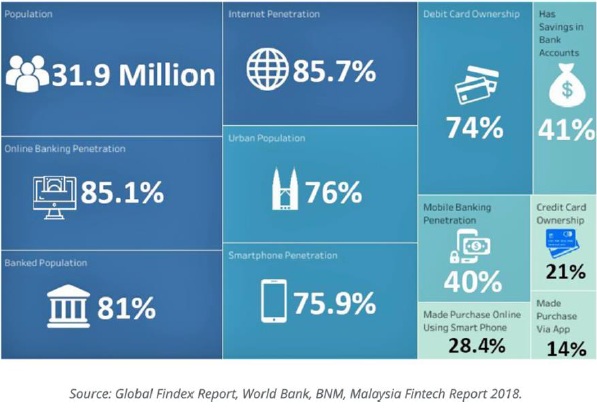

In fact, Ernst & Young’s (EY) Asean FinTech Census 2018 dubbed Malaysia an “emerging fintech hub in Asia”, with US$75 million (RM308 million) worth of investments made in 2017 — a 15 times increase year-on-year. In Malaysia there are 26 commercial banks, 16 Islamic banks, one international Islamic bank, 11 investment banks and from the total 26 commercial banks, 18 are foreign-based lenders. There are 196 key fintech players in Malaysia as of 2019 with 38% in e-wallet and payment, according to the Fintech Malaysia Report 2019.

On 27 December 2019, Bank Negara Malaysia released an exposure draft for Licensing Framework for Digital Banks, developed with the intent to offer banking products and services to underserved or unserved market through digital means. The hope is that the framework will play a key role in achieving Malaysia’s Shared Prosperity Vision (SPV) 2030. Hot off the heels of digital banking legislation trotted out by other Asian Pacific countries, Bank Negara Malaysia is even strongly considering issuing up to five digital bank licences.

Banking Culture in Malaysia

Hong Leong Bank – As Malaysia’s oldest home-grown bank, Hong Leong Bank adopted the mantra ‘digital at its core’ as a way to embrace the digital era. The hope is that best digital practices will be adopted in the way their departments are run, the way they collaborate and the workplace overall even while the core banking systems remain the same. Because digital transactions now account for the bulk of their total transactions, most of branch staff now have to directly engage with customers. Digitalization presents an opportunity for more personal user experience and enhanced opportunities to cross-sell Hong Leong products, thus transforming not only the customer experience, but middleware and back-end systems as well.

Citibank – Leading a digital workforce requires leadership who can adapt and change with the times. Citibank’s CEO emphasises four distinct traits; “Clear direction, good communication, empathy and the ability to lead from the front.” Attracting and keeping their majority millennial workforce requires a collaborative and innovatice culture which promotes opportunities to develop new skill sets and leadership qualities. Training programmes are abundant as are task forces, special groups and digital councils where ideas can flourish in the digital space.

Does Culture matter on the bottom-line dollar?

Since the 2008 Financial Crisis, the banking industry “has made significant efforts to understand and improve the culture of their firms, and scrutinize employee conduct,” according to the Group of Thirty (G30) “Banking Conduct and Culture: A Permanent Mindset Change,” report. More significantly is the fact that an estimated US$350-US$470 billion in penalties (including fines and litigation / settlement charges) had to be paid by the banking industry for conduct-related matters.

Besides monetary losses, discounting the building blocks of culture and trust can lead to concerns in:

1. a lack of faith that the industry has really changed its way

2. potential for conduct and culture fatigue

3. “employee burnout from all of the culture and conduct initiatives,”

4. a desire “to get back to business”

5. uncertainty around new developments (such as technology and artificial intelligence)

6. fear that the ongoing organizational changes are not fully embedded and won’t “stick” in the longer term

“Only by making culture stewardship a permanent and integral part of how business is conducted will organizations avoid culture fatigue and backsliding,” the report stresses.

Financial technology has displaced the over decade-old 2008 financial crisis as the main issue driving the international regulatory agenda. Success in the digital age will in fact heavily rely on overcoming functional and departmental silos, a fear of taking risks and difficulty forming and acting on a single view of the customer.

Raising an organization’s digital quotient are only the first few steps in a digital transformation journey. In the short run, their competitiveness will be defined by how much push and support they give their employees with professional development. To remain resilient for the next recession or financial crisis, banking leadership need to look for strategic breakthrough opportunities, even innovations from their employees that can lay the foundation of future business models and processes.

The overhyped agile approach to developing and delivering technology can itself become a sacred cow, creating a culture of short termism and temporary fixes – often obstructing longer-term scaling – the very thing the agile philosophy and culture is supposed to help firms avoid. Banks cannot break the wheel of decades-old legacy systems overnight. Handelsbanken certainly didn’t, they just adopted what complemented their way of work and applied the technology to their operations without alienating their people. Really, banks could learn a lot from up-and-coming Fintechs, how these new start-ups operate on a daily basis, how the new generation relate to their employees and what is their view on customer experience, not just focused on products and services. At the same time, Fintechs have a bottomless well of knowledge to learn from incumbents as well, so they can become more valuable partners to them. Collaboration, not competition, will be key.

Culture is very much like trust – challenging to build, easy to break and even harder to change. Most important, the culture being built should resonate with the bank’s culture and drive them into high-performance action. Motivated employees, empowered with technology that help to reduce human error, save time from productivity-killing tasks and create more time to be proactive will bring true competitive edge to the financial industry.

For more information on how to build a data driven organization strategy, please visit https://www.thecads.com/